A lot of people think mobile car detailing insurance is just paperwork you keep in a glove box and hope you never use. That changes fast when a routine job goes sideways.

You're polishing a hood in a customer's driveway. The hose shifts, water sprays wider than expected, and now the open garage has a wet floor and a soaked tool chest. Or a client steps around your extension cord, slips on rinse water, and suddenly the conversation isn't about gloss levels or pet hair removal. It's about damage, responsibility, and who pays.

That is why mobile car detailing insurance matters. Skill prevents plenty of problems, but it doesn't stop every accident. Mobile work adds variables you can't fully control. Sloped driveways, tight parking areas, passing traffic, kids walking through the work area, changing weather, and customer vehicles that may be worth far more than your detailing rig.

For detailers, insurance protects the business you've built. For customers, it shows you're hiring someone who treats your property like a professional operation, not a weekend side hustle with a pressure washer and good intentions.

Why Your Detailer Needs More Than Just Good Wax

A good mobile detailer knows paint, interior materials, trim sensitivity, odor removal, and how to work efficiently on-site. That still isn't enough by itself.

The job doesn't happen in a controlled shop. It happens in driveways, office lots, apartment complexes, and fleet yards. Every location changes the risk. A rotary, DA polisher, extractor, pressure washer, hose reel, canopy, generator, and chemical kit all create exposure before a single panel gets cleaned.

Professional work brings professional risk

Customers usually notice the finish. They don't always notice what the detailer is managing in the background:

- Foot traffic around the job: Family members, neighbors, and delivery drivers may move through the work area.

- Property close to the vehicle: Garage doors, landscaping, walls, and parked cars sit within a few feet of hoses and tools.

- Unpredictable conditions: Wind can move towels and extension cords. Rain can interrupt a service. Heat can change how products behave on paint and trim.

- High-value assets: Even an ordinary appointment can involve a vehicle, driveway, and surrounding property that would be expensive to repair.

A polished result looks professional. Proper insurance proves the business is professional.

That's why insurance shouldn't be treated like an afterthought or a box to check for a website footer. It's part of operating correctly. Customers are trusting a detailer with a vehicle they rely on every day, and in some cases one they care about very much.

What customers should take from this

If you're hiring a mobile detailer, insurance isn't a rude question. It's a basic professionalism question. The same way you'd expect careful wash methods, clean towels, and proper products, you should expect real coverage that matches mobile work.

A detailer who invests in coverage is showing something important. They understand that accidents can happen even when the work is done carefully, and they've taken steps to protect both sides when they do.

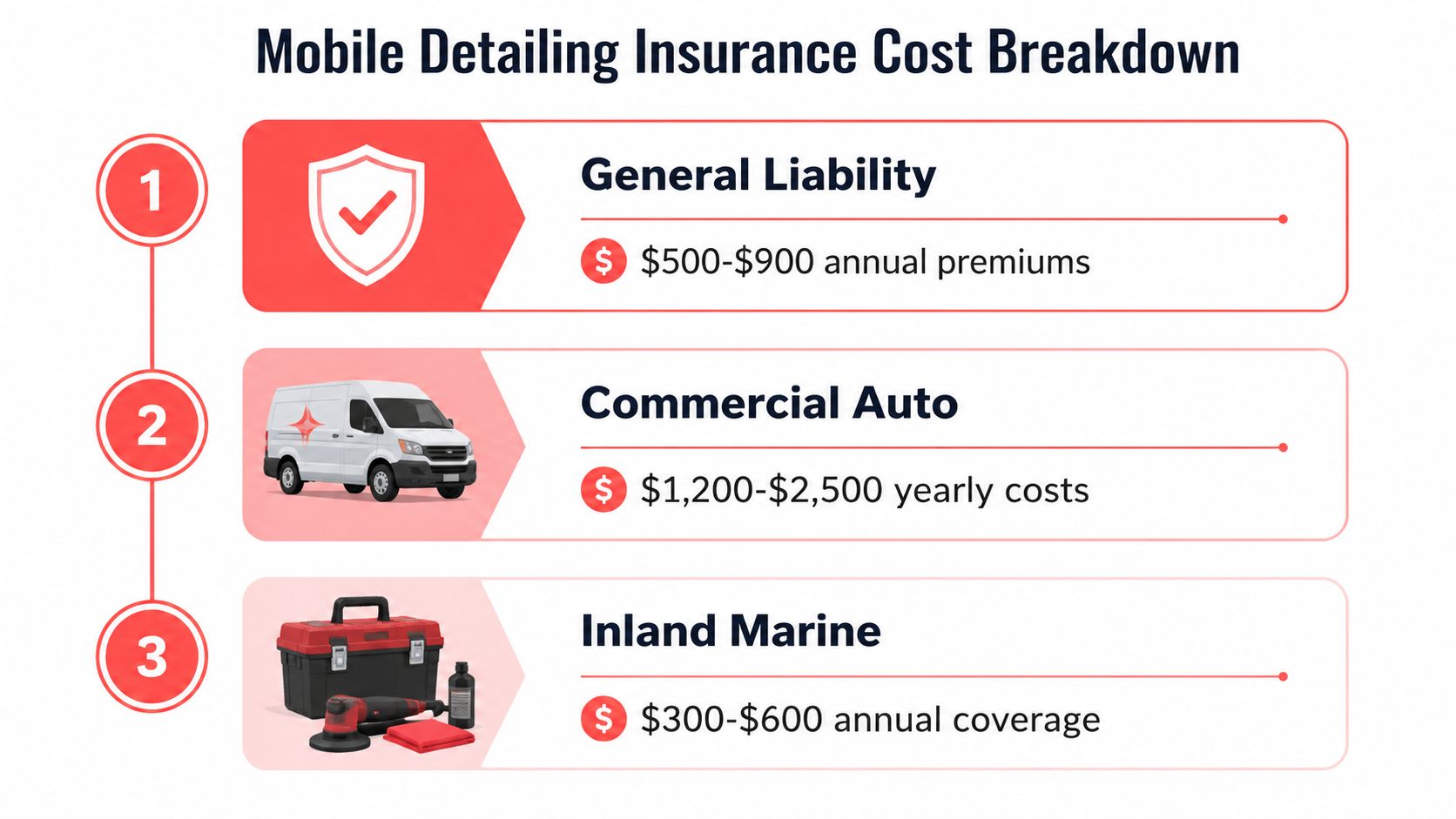

The Foundation General Liability and Commercial Auto

A pretty common Central PA scenario goes like this. A mobile detailer pulls into a driveway in Camp Hill or Mechanicsburg, unloads gear, starts setting up hoses and cords, and backs the van a little closer to the work area. In that one appointment, two separate exposures are already in play. One is what happens around the job site. The other is what happens on the road in the business vehicle.

That is why general liability and commercial auto sit at the base of the policy stack for mobile detailers.

General liability handles third-party injury and property damage

General liability applies when a customer, neighbor, or someone else outside your business is injured, or when you damage property around the vehicle. For mobile work, that can be a customer slipping near rinse water, a pressure washer line knocking over a planter, or a polisher cord scuffing a garage door frame while you reposition equipment.

This policy does not replace careful setup. It backs you up when careful setup still is not enough.

For detailers, the practical value is simple. One claim can wipe out months of profit if you are paying out of pocket. For customers, it means there is a real process for handling a mistake instead of an awkward argument in the driveway.

Commercial auto covers the vehicle used for the business

If the van, truck, or trailer is part of how you earn money, personal auto insurance may not fit the risk. That gap catches new operators all the time, especially the ones who are just getting started with a side hustle and assume a personal policy covers trips to customer jobs.

Insurance carriers usually look at how the vehicle is being used. Daily travel to appointments, stored equipment, signage on the vehicle, and hauling water tanks or generators all point to business use. If there is a crash on the way to a job in Harrisburg, York, or State College, you do not want to find out after the fact that your personal carrier is disputing coverage.

What detailers should check

For operators, start with a plain checklist:

- General liability that covers third-party bodily injury and property damage at customer locations

- Commercial auto for any van, truck, or trailer used to reach jobs or carry detailing equipment

- Proof of insurance you can send fast, because property managers, fleet clients, and careful retail customers ask for it

- Policy details that match how you work, including service area, vehicle type, and whether equipment stays in the vehicle overnight

If you are still building your operation, this guide on starting a mobile detailing business pairs well with getting your insurance set up correctly from the beginning.

What customers should ask before booking

Customers can protect themselves with a short screening process:

- Ask for a certificate of insurance, not just a verbal promise

- Confirm the business has general liability coverage for work performed on your property

- Ask whether the service vehicle is insured for business use

- If you have a tight driveway, HOA rules, or a high-value vehicle, mention that before the appointment so there are no surprises

That last point matters in Central PA, where many jobs happen in residential neighborhoods with narrow driveways, shared parking areas, and a lot of foot traffic. Good insurance does not make a detailer better at paint correction or interior work. It does show they are running a real business and planning for the risks that come with mobile service.

Solo operators should also look beyond the van and liability policy. Broader planning around health, liability, and disability insurance for pros can help protect the owner behind the business, not just the business assets.

Protecting Your Tools and Your Client's Car

A mobile detailer can do everything right on the paint and still get hit with a claim. A polisher gets stolen from the van overnight in Harrisburg. An extractor tips in a customer's driveway in Camp Hill and leaves damage on a door sill. A pressure washer hose catches a mirror in a tight suburban driveway. Those are everyday business risks, and the right policy setup needs to account for them.

The two coverages that usually fill the biggest gaps are inland marine insurance for mobile equipment and garagekeepers legal liability for customer vehicles in your care.

Inland marine covers the mobile workshop

A mobile setup is not just a van with some bottles in the back. It is a working shop that gets packed, unpacked, rolled across driveways, and left exposed during jobs. That changes the insurance problem.

Inland marine insurance is built for tools and equipment that travel. That can include polishers, extractors, vacuums, steamers, generators, hose reels, extension cords, canopy setups, and product inventory. If that gear is stolen, damaged in transit, or damaged at a job site, this is often the policy that responds.

For Central PA operators, that matters more than many new detailers expect. Jobs happen in residential neighborhoods, apartment lots, office parks, and dealership overflow areas. Equipment gets moved constantly, and the risk is not limited to theft. Rain, loading mistakes, tip-overs, and chemical spills can all turn into real losses.

Garagekeepers protects the customer's vehicle itself

This is the policy many detailers skip until they understand what general liability does not cover.

Once a customer's car is in your care, custody, and control, damage to that vehicle often falls outside standard general liability. Garagekeepers legal liability is the coverage designed for that exposure. If a rotary burns an edge, a steamer affects a screen, a bottle leaks onto leather, or a vehicle gets damaged while positioned for service, this is the policy that may step in.

For a professional mobile detailer, garagekeepers coverage should be considered required. Customers should ask about it too, especially if they own a newer vehicle, a luxury car, or anything with expensive trim, glass, or electronics.

For anyone comparing policy language, this overview of garagekeepers liability coverage is a helpful reference because it explains why a business needs separate protection for property that belongs to someone else but is temporarily under its control.

Here's a useful walkthrough on the subject:

Where detailers get this wrong

The usual mistakes are simple, but expensive:

- Assuming general liability covers the client's car: It often does not once you are actively servicing the vehicle.

- Underinsuring tools: Replacing one polisher is manageable. Replacing an extractor, generator, pressure washer, and full chemical stock at once is a different problem.

- Ignoring off-site exposure: A policy written around a fixed location can leave gaps for mobile work.

- Skipping condition photos: Before-and-after photos help settle disputes about pre-existing scratches, cracked trim, stained fabric, or failing clear coat.

Customers can use this section as a quick screening tool. Ask your detailer what protects the vehicle while it is being worked on, and ask what covers the equipment being brought onto your property. A serious operator should answer clearly.

For detailers, the practical test is simple. If your van was broken into tonight, or if a customer's vehicle was damaged during tomorrow's appointment, would your current insurance handle the loss without putting your cash flow or reputation at risk? If the answer is unclear, the policy needs work.

Insuring Your Team and Your Reputation

A common turning point for mobile detailers in Central PA looks like this. One van turns into two. A part-time helper becomes a real employee. Then a routine job in State College or Camp Hill turns messy because someone slips on wet pavement, strains a back pulling an extractor, or says the wrong product was approved for a delicate interior surface.

At that point, insurance is no longer just about the van, the tools, or the car in front of you. It is also about payroll, hiring, training, customer communication, and whether one mistake follows your business name for the next two years.

Workers' comp starts when you stop working alone

If you hire employees, workers' compensation usually moves into the required category under state rules. That matters in detailing because the injuries are rarely dramatic, but they are common enough to disrupt a small operation fast.

Crews lift water tanks, polishers, and generators. They work in driveways, parking lots, and shaded spots that stay slick longer than expected. They kneel, bend, reach, and repeat the same machine motions all week. A shoulder strain or slip-and-fall can put a technician out of work and put the owner in a bad position if coverage is missing.

For detailers, the checklist is simple:

- Confirm whether everyone helping on jobs is classified correctly

- Make sure mobile work is included, not just work at a fixed shop

- Keep training records for safe chemical handling, lifting, and machine use

- Report injuries quickly and document what happened

Customers can take a lesson from this too. If a company sends a team to your home, ask whether its workers are covered while on your property. A professional operator should be able to answer without hedging.

Professional liability covers service judgment

Detailing is hands-on work, but it also involves judgment. Should a stain get aggressive treatment or a safer first pass? Is steam appropriate around aging trim? Is a heavy compound worth the risk on thin paint? Can an odor treatment be used safely around child seats, electronics, or sensitive materials?

Those choices can trigger disputes even when there is no obvious accident. Professional liability, often called errors and omissions coverage, can help when a customer claims your advice, recommendation, or process caused a loss.

This matters more as services get more specialized. Ceramic coatings, odor removal, paint correction, overspray removal, and stain treatment all carry a higher expectation that the operator knows where the line is. Customers are paying for results, but they are also paying for restraint.

Cyber risk is real for a mobile operation

Many mobile detailers run the whole business through a phone. Booking requests, saved addresses, card payments, invoices, text threads, and vehicle photos all live in digital systems. If that information is exposed, locked up, or misused, the problem is no longer limited to one job.

Cyber coverage can help with data breaches, payment issues, and the cleanup that follows a hacked account or compromised device. For a small business, the bigger hit is often reputation. Customers trust you with their address, schedule, contact details, and sometimes gate codes or garage access notes. Losing control of that information can cost repeat business fast.

A practical protection stack for a growing mobile detailing company often includes:

- Workers' comp for employee injuries and lost-wage obligations tied to job-related incidents

- Professional liability for disputes tied to recommendations, methods, or service decisions

- Cyber coverage for customer data, payment systems, scheduling platforms, and phone-based business operations

For detailers, growth means more than booking more cars. It means setting up the business so one employee injury, one disputed recommendation, or one hacked payment account does not wipe out a season's profit.

For customers, the takeaway is just as direct. If your detailer has a crew, handles digital payments, and offers specialized services, ask what backs up those promises. A serious business protects the work, the workers, and your trust.

Decoding Policy Costs and Coverage Limits

A mobile detailer in Central PA can go months without a claim, then lose a chunk of the year's profit on one mistake. A pressure washer tip cracks a trim piece in State College. A hose catches a customer's garage light in Camp Hill. A van loaded with polishers and extractors gets hit on the way to a job in Hershey. Insurance pricing makes more sense once you measure it against jobs like that.

What the core policies usually cost

For many small mobile operations, general liability, commercial auto, and a business owner's policy are usually within reach. The exact premium depends on your vehicle, service area, claims history, and whether the carrier is writing for mobile work instead of a fixed shop model.

A BOP can be a practical fit for a smaller setup that wants liability and property coverage under one policy instead of stacking separate policies from scratch. It is not automatically the best value. If your tools are constantly off-site and your main exposure is tied to road use and customer vehicles, a bundled policy still needs close review.

Here's the simple breakdown.

| Insurance Type | What It Covers | Who Needs It |

|---|---|---|

| General Liability | Third-party bodily injury and property damage | Every mobile detailer |

| Commercial Auto | Business-use vehicles transporting equipment and traveling to jobs | Any operator using a vehicle for work |

| Business Owner's Policy | Bundled liability and commercial property protection | Small operators wanting broader bundled coverage |

For customers, this matters too. If a detailer says, “I'm insured,” ask what kind. A policy that covers a home office but not a work van, mobile setup, or customer property does not answer the real risk.

What coverage limits mean in real life

Coverage limits are where a policy either holds up or comes apart.

- Per occurrence is the maximum the policy may pay for one covered claim.

- Aggregate is the maximum it may pay across the full policy term.

If a liability policy shows a per-occurrence limit and an aggregate limit, the first number applies to a single incident. The second applies to the total paid out before renewal. That distinction matters for busy operators who may complete several jobs a day during the spring and fall rush in Central PA.

One serious claim can test the first number. Multiple smaller claims in the same year can eat into the second. That is why the cheapest quote on the page is not always the safer choice.

Why one quote can look very different from another

Insurers price the operation in front of them, not the label on the business card.

A solo detailer doing light interior work in a small radius around Mechanicsburg can look very different from a crew running paint correction, engine bay cleaning, odor treatment, and fleet work across Harrisburg, York, and Lancaster. Add a wrapped van, a trailer, more expensive equipment, or prior claims, and the premium can shift fast.

Common pricing factors include:

- Vehicle use: Daily driving, loaded equipment, and higher mileage usually increase exposure.

- Service mix: Higher-risk services can change how an insurer views the account.

- Territory: Tight residential driveways, apartment lots, commercial properties, and winter road conditions all affect risk.

- Claims history: Prior losses often raise premiums or narrow carrier options.

- Equipment storage: Locked vehicles, secure storage, and documented inventory can help support a better quote.

Cheap insurance with the wrong exclusions is a bad buy.

For detailers, the smart question is whether the policy fits the way the business operates. For customers, the smart question is whether the detailer carries enough coverage to make a problem right if something goes wrong.

How to Get Insured and Lower Your Premiums

A mobile detailer finishes a correction job in Camp Hill, packs up, and heads to the next stop. On the way, a shelf tips in the van, a polisher cracks, and a gallon of chemical leaks into a tote of towels and cords. The right policy setup turns that into an insurance call and a cleanup job. The wrong setup turns it into an out-of-pocket hit.

Getting insured starts with describing the business the way it runs on the road in Central PA. Carriers price what you do every week, not what you hope to do later.

Start with your real operation

Before you ask for quotes, write out the details that change coverage and pricing. A vague application usually gets a vague quote.

Include:

Your actual service list

List the work you perform now, such as interior detailing, paint correction, engine bay cleaning, odor treatment, stain extraction, ceramic coating prep, or headlight restoration.Your mobile setup

Note whether you run from a van, pickup, trailer, or a mixed setup, and whether water tanks, generators, or shelving are permanently installed.Your equipment inventory

Count the gear that would hurt to replace tomorrow. Polishers, extractors, vacuums, pressure washers, steamers, canopy setups, extension cords, and chemical stock all matter.Your service area and job sites

Driving from Mechanicsburg to Harrisburg, York, Carlisle, or Lancaster creates different exposures than staying in one zip code. Apartment lots, office parks, and tight residential driveways also change the risk.

A newer operator should keep this in a simple spreadsheet. An established shop should update it every time gear or services change.

Compare policies by fit

Price matters. Fit matters more.

Ask the agent or broker direct questions about how the policy applies to mobile detailing, off-site equipment, and customer vehicles connected to your work. If the answers sound generic, keep asking. A policy that fits a fixed-location shop can miss common mobile exposures.

Useful questions include:

- Does this policy match mobile detailing operations performed at customer homes and businesses?

- What exclusions apply when I work on someone else's property?

- Are my tools covered while stored in the vehicle and while in use off-premises?

- Is damage tied to my work on a customer vehicle addressed somewhere in this insurance package?

- Do I need any endorsements for higher-risk services or chemical storage?

For detailers, that checklist helps avoid expensive blind spots. For customers comparing providers, it is one more reason to hire a company that can explain its coverage clearly, the same way it should explain its wash process, correction plan, or mobile detailing service options near you.

Practical ways to lower premiums

Insurance gets cheaper when the business is easier to underwrite and less likely to produce a claim.

Start with the habits that reduce disputes and losses in the first place. Photograph the vehicle before service. Photograph it again after service. Keep a signed service agreement. Use written check-in notes for existing scratches, cracked trim, loose badges, and delicate aftermarket parts. Those habits help with claims, and they also show an insurer you run a controlled operation.

Other steps often help:

- Bundle policies where it makes sense: A business owner's policy can reduce cost for smaller operations that need liability plus business property coverage.

- Keep driver records clean: Tickets and accidents push commercial auto pricing up fast.

- Secure equipment every day: Locked vans, alarm systems, cable locks, and organized shelving reduce theft and damage risk.

- Train to one process: Consistent wash, chemical handling, ladder use, and loading procedures lead to fewer preventable mistakes.

- Report the business accurately: If you are mobile, insure it as a mobile operation. Misclassifying the business can create claim problems later.

- Review limits yearly: Growth changes exposure. A solo detailer and a two-truck crew should not carry the same setup by default.

One more practical point for both sides of the transaction. Keep your certificate of insurance current and easy to send. Customers in Central PA are asking for proof of coverage more often, especially for higher-end vehicles, fleet work, and apartment or HOA properties. If you need a plain-English reference on how to verify a COI, send that along with your certificate and save everyone time.

The detailers who get better insurance value usually present a clean, well-documented business. The customers who hire them get something valuable too. Fewer surprises if a job goes sideways.

A Customer Guide to Vetting Your Detailer

Customers don't need to become insurance experts. They just need a short checklist and the confidence to ask.

A professional detailer shouldn't be bothered by that request. If anything, it gives them a chance to show they run a real business.

What to ask for

The simplest document is a certificate of insurance, often called a COI. It gives you a snapshot of active coverage.

When you ask, keep it straightforward:

“Before we schedule, could you send over your certificate of insurance so I can confirm coverage for mobile detailing work?”

That isn't confrontational. It's normal.

What to review on the COI

Look for a few practical details:

- Active policy dates: Make sure the policy is current on the day of service.

- Business name match: The insured business name should match the company you're hiring.

- Relevant policy types: General liability is the baseline. For mobile work involving hands-on vehicle service, customers may also want confirmation that customer vehicles are properly addressed within the business's coverage setup.

- Operations fit: The business should be insured for the kind of work it performs.

If you've never checked one before, this guide on how to verify a COI gives a useful overview of the process.

Other signs you're hiring a pro

Insurance is the main filter, but it's not the only one. Pair it with a few common-sense checks:

- Service clarity: The detailer should explain what's included and what isn't.

- Professional communication: Scheduling, arrival windows, and payment terms should be clear.

- Real local presence: Reviews, service-area information, and business details should line up.

- Appropriate service recommendations: A good detailer won't push risky shortcuts or one-size-fits-all fixes.

If you're comparing providers, this article on finding the best car wash and detail near you can help you evaluate professionalism beyond price alone.

Customers often focus on convenience, and that makes sense. But the best mobile service isn't just convenient. It's accountable.

Ready for a Worry-Free Detail Experience

A clean vehicle is the visible result. Peace of mind is the part most customers don't think about until something goes wrong.

That's why mobile car detailing insurance matters so much. It protects the business, protects the customer, and sets a clear line between a professional operation and someone working out of a trunk. The right coverage supports the work, the vehicle, the equipment, and the trust behind the appointment.

If you're hiring a detailer, ask better questions. If you're running a detailing business, insure the work you do. And if you want a better idea of what professional detailing service should include, review what a full detail includes before you book.

If you're in Central Pennsylvania and want the convenience of mobile detailing without the uncertainty, book with The Mobile Buff. We serve drivers in the Harrisburg area and surrounding communities with professional on-site detailing, careful workmanship, and the kind of insured, customer-first service serious vehicle owners expect. You can also check our local presence and reviews on our Google Business Profile.